AN EFFECTIVE REGULATION CAN STIMULATE BANKING ACTIVITIES BY AGENTS IN WEST AFRICAN ECONOMIC AND MONETARY UNION (WAEMU)

The West African Economic and Monetary Union (WAEMU) took important steps towards financial inclusion in recent years.

The mobile money has contributed to this progress in the context of regulations that allows mobile networks operators to offers electronic money services and expands their agent’s networks as well as these scope of services.

However, the West African Economic and Monetary Union (WAEMU) regulations make it difficult for Banks and microfinance institutions deploying their own agent’s networks and their full contribution to financial inclusion. While the accounts numbers and mobile money agents in the region has almost doubled between 2014 and 2017 (36, 4 million and 183 000 respectively), Banks and Microfinance Institutions are still behind this.

“THE MICROFINANCE CAN AND SHOULD TAKE A BETTER PLACE IN THE AFRICAN FINANCIAL SECTOR”

Advans in Ivory-Coast recently announced its decision to inject 1.000 Billion of CFA almost 1.5 Billion of Euro in the Ivorian economy from now to 2023.

In this interview granted to the “Africa Forum” the managing director of this institution Mr Gael Briot highlighted the credit supply distribution mechanisms, their priority in the funding strategy of the Ivorian SME and major challenges in this growing sector in Africa. To capture opportunities of African markets, the group also present in Tunisia, Cameroon, Ghana, Nigeria, DRC has developed a wide range of products, services and intend to double the number of their 350 000 clients and 2 700 African employees in the coming years.

TRAINING ON DIGITAL FINANCE IN DRC

As part of its capacity building activities, Microfinance African Institutions Network (MAIN), in collaboration with GAMF organized in Bukavu in DRC, from 4-8 June 2018, a sub- regional training on “Digital finance in MFI”

The training gathered 34 participants (31 men and 03 women) coming from Tchad, Burundi, and DRC from the 18 Institutions.

The training was opened by the financial advisor of the governor of South-Kivu.

Ten modules were delivered during the session. What gave to participants the overview of the opportunities that Digital finance could bring to MFI. The training gave a unique opportunity to participants to have tools and knowledge to enable them to launch digital finance projects in their institutions.

The practical case studies have reinforced the understanding of participants.

The training evaluation showed the general satisfaction from participants who found the session very rich and practical.

The closing of the session was done by the chairman of MAIN who urged participants to make good use of the learning outcomes of the training.

TESTIMONY FROM A PARTICIPANT

Question : Can you tell us who you are? (Your name, which institution you are coming from, the country and the department in which you are working) and also what motivated your participation to this session

Réponse : I’ am Joyce Hakizimana Managing Director of Fonds de Micro Crédit Rural (FMCR) in Burundi.

The FMCR, organization which I managed is public (i.e. establish by the government of Burundi) with the aim of facilitating access to credit for rural actors.

Our institution grants loan to microfinance institutions through a micro credit facility and a guarantee fund. We also have a role to train and raise awareness on financial inclusion and gives technical assistance.

The FMCR is the umbrella of the MFI in refinancing. Through this training, I am looking forward to using digital finance in our refinancing procedures. This won’t be possible if we do not have sufficient knowledge in the field of digitalization.

Question : What have you learned during this session?

Réponse : So many things where taught during this training. Among them:

First of all, the proper definition of what we call Digital finance which is financial services having as support digital technology.

Then, the value added of digital finance for an MFI and why not for FMCR once implemented.

Also the possible Business Models (BA) when an MFI decided to migrate to the digital finance strategy, which business model should suite the MFI? Be able to do the SWOT analysis for each business model and see what can be applied to my institution.

Finally the different steps in implementing a digital finance project in a microfinance institution.

Question : How will this training be beneficial or useful in your daily works?

Réponse : With the mission of FMRC, this training will help in terms of decision making. Make a choice of a business model to be presented based on the SWOT analysis.

First convince the different decision bodies from the bottom to the top: Executive committee, board members, and the affiliated ministry.

Question : What are your impressions about this training, would you recommend this to one of your colleague?

Réponse : This Training comes at the right time, to meet a need of the FMCR. The world is changing as technology changes. The MFI is getting closer to their target through the use of mobile phone.

This training will improve the financial services of the MFI. It’s also advisable to develop a business model that is well suited to refinancing microfinance institutions.

The exchanges between the facilitators and the participants have been very rich and I will not hesitate to recommend this training to any of my colleague. Thanks to MAIN for organizing this training and for inviting the FMCR.

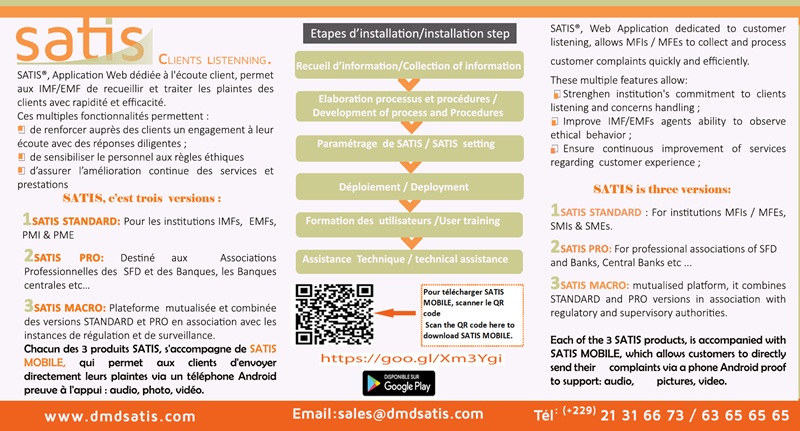

COMPLAINT MANAGEMENT TOOL

UPCOMING EVENTS

14th edition of the annual MFT boulder microfinance training program

Type: training

Lieu : Turin, Italy

Date : 23rd July 2018 – 03rd August 2018

Training program at Uganda Martyr University (UMU)

Type : training

Lieu: Ngozi, Uganda

Date: 23 July 2018- 04 August 2018

Training on Savings mobilization

Type: training

Lieu: Addis, Ethiopia

Date: 13-16 August 2018

Training program at Université Catholique d’Afrique Centrale (UCAC)

Type: training

Lieu : Yaoundé, Cameroon

Date: 13 August- 02 September 2018